On Wednesday, June 10, 2020, the AICPA published Technical Questions and Answers (TQA) 3200.18, Borrower Accounting for a Forgivable Loan Received Under the Small Business Administration Paycheck Protection Program providing guidance on the accounting for loan forgiveness under the Paycheck Protection Program (PPP).

The TQA provides borrowers guidance in accounting for the forgiveness.

Option 1:

Record the advances as a liability classified as a loan on the balance sheet. Once the PPP Forgiveness application has been submitted and approved, extinguish the liability.

“Regardless of whether a nongovernmental entity expects to repay the PPP loan or believes it represents, in substance, a grant that is expected to be forgiven, it may account for the loan as a financial liability…”

“The proceeds from the loan would remain recorded as a liability until either (1) the loan is, in part or wholly, forgiven and the debtor has been “legally released” or (2) the debtor pays off the loan to the creditor. Once the loan is, in part or wholly, forgiven and legal release is received, a nongovernmental entity would reduce the liability by the amount forgiven and record a gain on extinguishment.”

The journal entries would be as follows:

This example assumes the full PPP loan has been forgiven in whole. Any amounts not forgiven would remain as a liability until paid in full.

Option 2:

Record the advances as a liability classified as a deferred income liability. Reduce the liability as it incurs the related costs to which the loan relates (i.e. compensation expense).

“If a….business entity……expects to meet the PPP’s eligibility criteria and concludes that the PPP loan represents, in substance, a grant that is expected to be forgiven, it may analogize to IAS 20 to account for the PPP loan.”

“Under this model….once there is reasonable assurance that the conditions will be met (i.e. forgiveness will occur either in part or in full), the earnings impact of government grants is recorded “on a systematic basis over the periods in which the entity recognizes as expenses the related costs for which the grants are intended to compensate.”

“A business entity would reduce the liability, with the offset through earnings (presented as either [1] a credit in the income statement, either separately or under general heading such as “other income,” or [2] a reduction of the related expense), as it recognizes the related cost to which the loan relates, for example, compensation expense.”

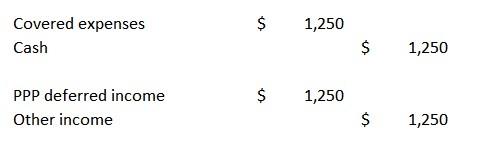

The journal entries would be as follows:

OR

This example assumes that at the end of week one, $1,250 of covered expenses have been incurred. This example also assumes the entity will apply for and expect to receive full forgiveness after eight weeks.

If you are a nonprofit entity, there is one other option available to you that would, in essence, reflect the PPP proceeds as a conditional contribution.

Entities must also adequately disclose their accounting policy for such loans and the related impact to the financial statements.

If you need assistance navigating the PPP Forgiveness accounting or any other aspects of the PPP, please reach out to your DHJJ CPA.